MOL Group Upstream

We have more than 85 years of experience in oil and gas exploration and production and our diverse portfolio consists of assets in 9 countries with production activity in 8 countries.

We are committed to the key principles of sustainable operation. We strive for zero HSE incidents and protection of the environment by eliminating spills, decreasing greenhouse gas emissions and participating in the World Bank’s Zero Flaring Initiative.

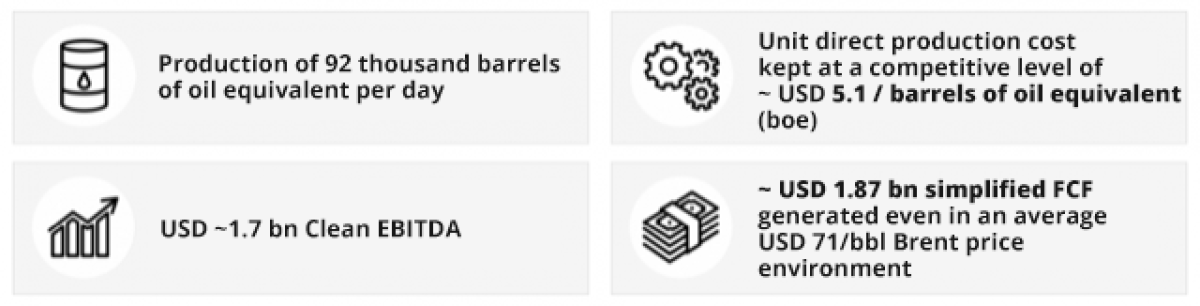

2023 IN FIGURES

KEY FACTS

OUTLOOK FOR 2025-2030 based on 2030+ Strategy

-

Segment level production to be delivered at 90 or higher MBOEPD

-

Keep unit direct production cost in the competitively low range of USD 6-8/boe

-

To spend USD 2 bn as organic CAPEX

-

Launch new Low Carbon projects in the CEE region